- Tel: 082 923 3151

- Email: jacobus@hfmdirect.co.za

A financial plan is a blue print of how you will build, develop and protect your lifestyle.

It is a map of how you will achieve your lifestyle goals through investments, financial products and insurance. It is a comprehensive analysis that looks at your current situation, helps establish your goals and formulates a plan on how to achieve them.

A good financial plan considers factors such as how to best maximise your opportunities to save tax, how to build wealth and capital and how best to protect your assets and dependents.

It also takes into account your appetite for risk, how much time you have to achieve your goals, your current assets, liabilities and expenditure and important life events that may be taking place or approaching.

No two family’s lives or lifestyles are the same, so, it stands to reason a “one-size-fits-all” insurance or investment product will, in almost all cases, not meet your family’s specific requirements and objectives.

At HFM we recognise your situation is unique and that your life, circumstances and lifestyle is ever-changing. A financial solution that meets your particular needs today, may well not be appropriate in the future and YOU and your family need to have the control to make adjustments when necessary.

A young, married person, will want to protect his/her lifestyle in ways that are different from those of a single person, or perhaps someone else whose children have left home and is nearing retirement.

So what is the Lotto Effect? Very simply, many people who win a jackpot at the Casino or a Lottery suddenly find themselves “rich”. The sad state of affairs is they are not financially astute enough to handle their newfound “wealth” and this inevitably leads to the lucky winner destitute in a few short years.

After the lucky winners’s windfall, friends and family make demands and attempt to influence the lucky on to part with some or most of their winnings. The lucky one often resigns from their job or decides to set up a business they are ill equipped and prepared to run that unfortunately results in failure. In many instances assets are acquired and no forethought is given to the running costs or maintenance of such assets or the fact the fortune they have spent on the fancy car is money squandered as it depreciates faster than a Zim dollar.

We could carry on and on at the folly of the uninitiated yet the scenario painted above plays itself out every time the proceeds of a policy pay out to a beneficiary in terms of the policy. Think long and hard about this. If the beneficiary who is nominated to receive the proceeds of a policy, is the spouse or a child or any other person for that matter, are the beneficiaries capable of responsibly dealing with the proceeds of the policy or any asset that they may inherit??

Simple question! Simple solution! Trust owned policies are the ONLY way to ensure that your meticulous financial needs analysis and plan with your client will be carried out.

This is a CALL TO ACTION! Ensure that your clients protect their beneficiaries from themselves until they know how to handle the cash and assets they will inherit.

Debt can be crippling and affect all aspects of your life, happiness and health. Debt is also expensive and keeps you from reaching your financial goals. Settling it should be your top financial priority.

If you do not manage your debt properly you could be declared insolvent, something that will affect and make your financial life difficult for years to come.

Do not ignore your debts or your creditors! Pretending they are not there will not make them go away. If you are struggling to get out of debt seek professional advice. The National Credit Act provides consumers with ways to seek relief and assistance. More details can be found on the National Credit Regulator website.

You are in debt if you cannot meet your monthly payments and expenses including, credit cards, accounts, housing bonds, vehicle repayments and personal loans.

Make a firm decision that you will do what is required to get out of debt, formulate a plan and stick to it.

You should have life insurance if anyone depends upon you financially, a spouse, children or aged parents, for example. Perhaps you are helping to pay for a brother or sister’s university studies or have guaranteed a car or personal loan.

If you were to suddenly die, the people you help and care for now may find themselves facing a precarious financial situation. In addition, the value of your estate could be dramatically reduced, as assets you’ve built up are disposed of to pay creditors and settle outstanding taxes.

You should also own life assurance if you have any hire-purchase or lease agreements, are paying a bond or have any unsettled personal loans.

But it is not only formally employed people who should have life insurance cover. If you stay at home and provide services such as cooking, cleaning and child care for your family, you are making an enormous contribution. If you were suddenly removed, those left behind would have to make alternative arrangements in order to keep the family functioning.

Invariably those adjustments come with a price-tag. Children may have to be put into nursery schools or after-school care facilities, additional house-help might have to be hired and new transportation arrangements made — and that is the “best case” scenario!

Without the financial means to cope with your loss, the impact on your family could be devastating. They may be forced to uproot and move to a more convenient location that is closer to schools and facilities. In some cases there may be no option but to enrol children in a boarding school and to cut back on facets of their lives that they are used to.

You may work in the home but do not under estimate the financial contribution you make. As a partner and contributor to the financial well-being of your family, you also need life insurance.

Older couples also need life assurance to protect the surviving spouse and ensure that savings and retirement funds are not depleted by unexpected medical or other expenses.

The simple fact is, if you want a comfortable retirement you cannot leave the planning to someone else. If you sit back and hope that your company pension will somehow provide enough to give you the retirement you desire, you are likely heading for disaster. Research has shown that as many as 94% of South Africans do not make sufficient provision to enjoy a comfortable retirement. As a result, they need to continue working in their retirement years, or depend on family members for support.

The financial pressures to provide for a financially secure retirement are increasing because:

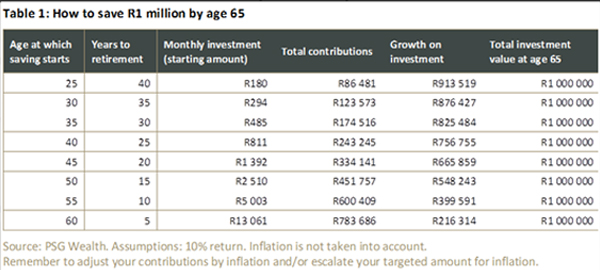

Putting off starting to build a retirement nest-egg is very costly indeed. The earlier you start making provision for your retirement, the better. The graph below illustrates how much you will need to invest at different ages to reach a goal of R1 000 000 at retirement. Please note that this is for illustrative purposes only. The graph is based on an investment return of 10% p.a. after charges.

Site Maintained and Designed by Ovation Internet